Automated FRS 102 lease accounting you can rely on

LOIS automates FRS 102 Section 20 compliance for UK and Irish organisations. Built on long standing IFRS 16 experience, LOIS supports consistent judgement, full audit traceability, and ongoing control as leases change over time.

FRS 102-ready from day one

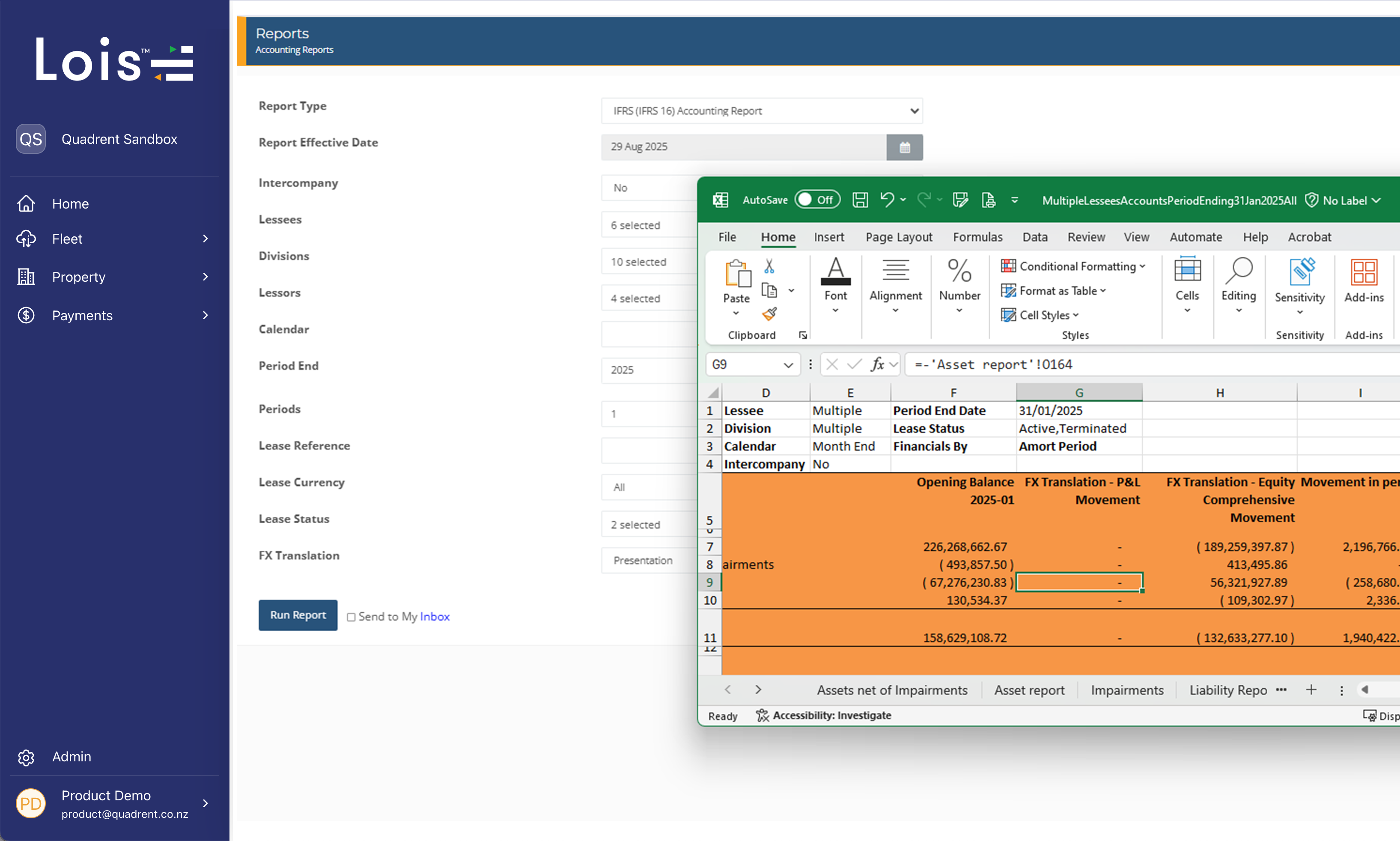

LOIS automates the full FRS 102 calculation set: right-of-use asset recognition, lease liability amortisation, depreciation and interest schedules, and disclosure reporting. No manual spreadsheets, no formula risk.

CA-qualified expert support

LOIS is built and supported by CA-qualified accountants with deep FRS 102 and IFRS 16 expertise. Our EMEA team has guided organisations through accounting standard transitions, providing practical guidance well beyond implementation.

Audit-ready every period

Every lease event, assumption change, and remeasurement is fully documented with a timestamped audit trail. LOIS locks periodic journals, reconciles the lease subledger to your general ledger, and produces disclosure-ready reports your auditors can rely on.

Effective 1 January 2026

FRS 102 is now in effect for periods commencing on or after 1 January 2026. Most UK and Irish entities are reporting under the new standard for the first time this year.

3.2 million entities affected

The FRC's 2024 impact assessment estimated 3.2 million UK and Irish entities fall under FRS 102. Any organisation holding property, vehicle, equipment, or other leases with terms over 12 months needs a compliant process now.

Balance sheet and EBITDA impact

Lease expenses now present as depreciation and interest rather than an operating cost. EBITDA rises, reported liabilities grow, and stakeholder narratives need to be managed before accounts are published.

Lessons from IFRS 16

LOIS guided organisations through IFRS 16, working alongside accounting firms during the transition. FRS 102 introduces the same complexity. The organisations that prepared early faced significantly less audit difficulty.

Everything your finance team needs for FRS 102 Section 20

FRS 102 calculations

Automated FRS 102 Section 20 calculations

LOIS handles every calculation FRS 102 Section 20 requires, with no manual input after setup. The platform computes right-of-use asset values, lease liability present values using the obtainable borrowing rate, depreciation and interest charges, and full amortisation schedules across every lease in your portfolio.

- Right-of-use asset recognition and subsequent measurement

- Lease liability amortisation using effective interest method

- Depreciation and interest split for P&L presentation

- Short-term and low-value asset exemption tracking

- Transition journal entries with no comparative restatement required

Lease lifecycle

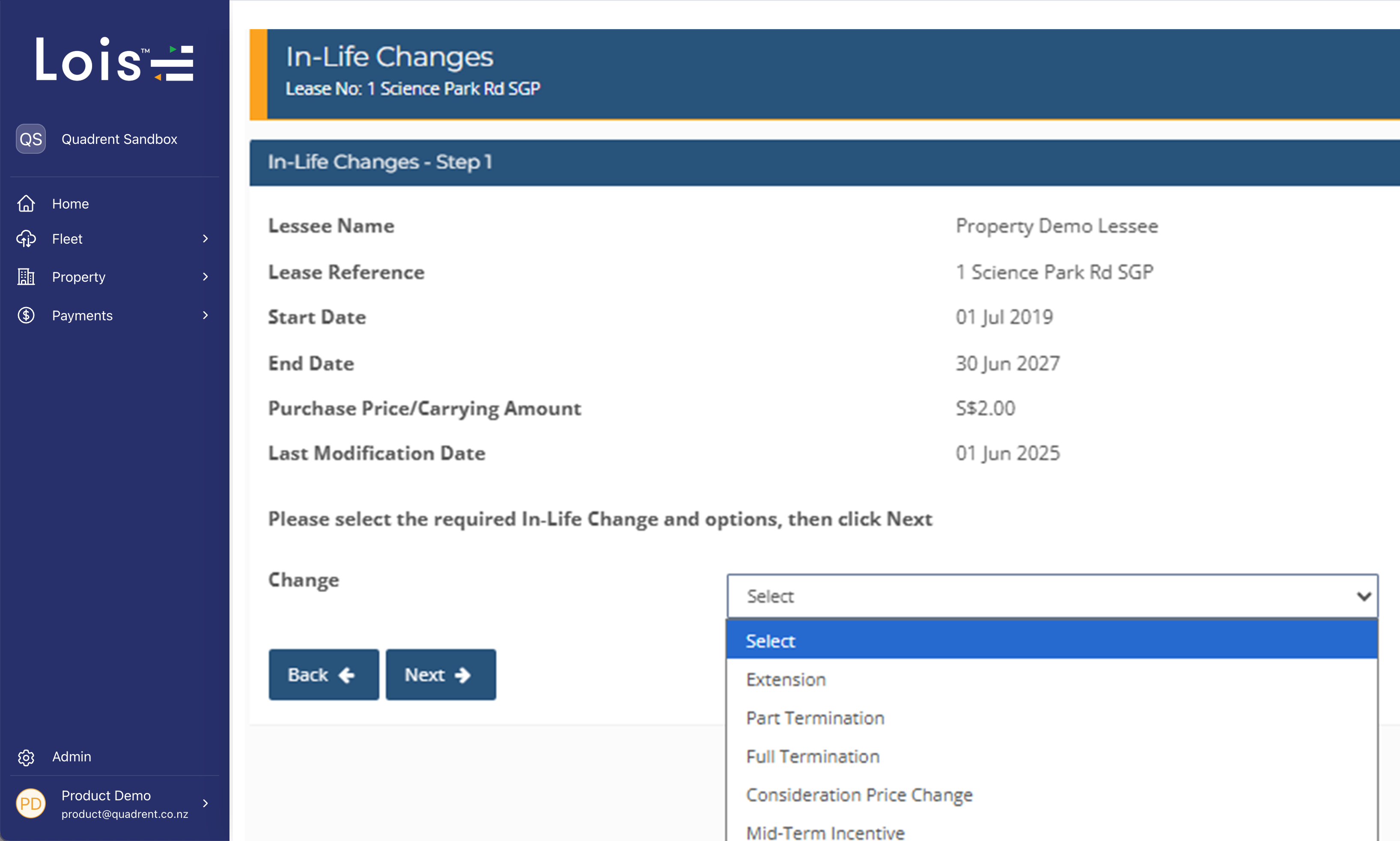

Full lease lifecycle and modification management

FRS 102 compliance is not a one-time exercise. Every rent review, extension, scope change, or early termination triggers a remeasurement. LOIS handles each modification automatically, recalculating schedules, generating updated journals, and maintaining a clear rationale trail for every judgement made.

- Extensions, part-terminations, and full early terminations

- CPI and RPI-linked rent review remeasurements

- Indexation and consideration changes

- Rental corrections and impairment records

- All modifications stored with timestamps for audit review

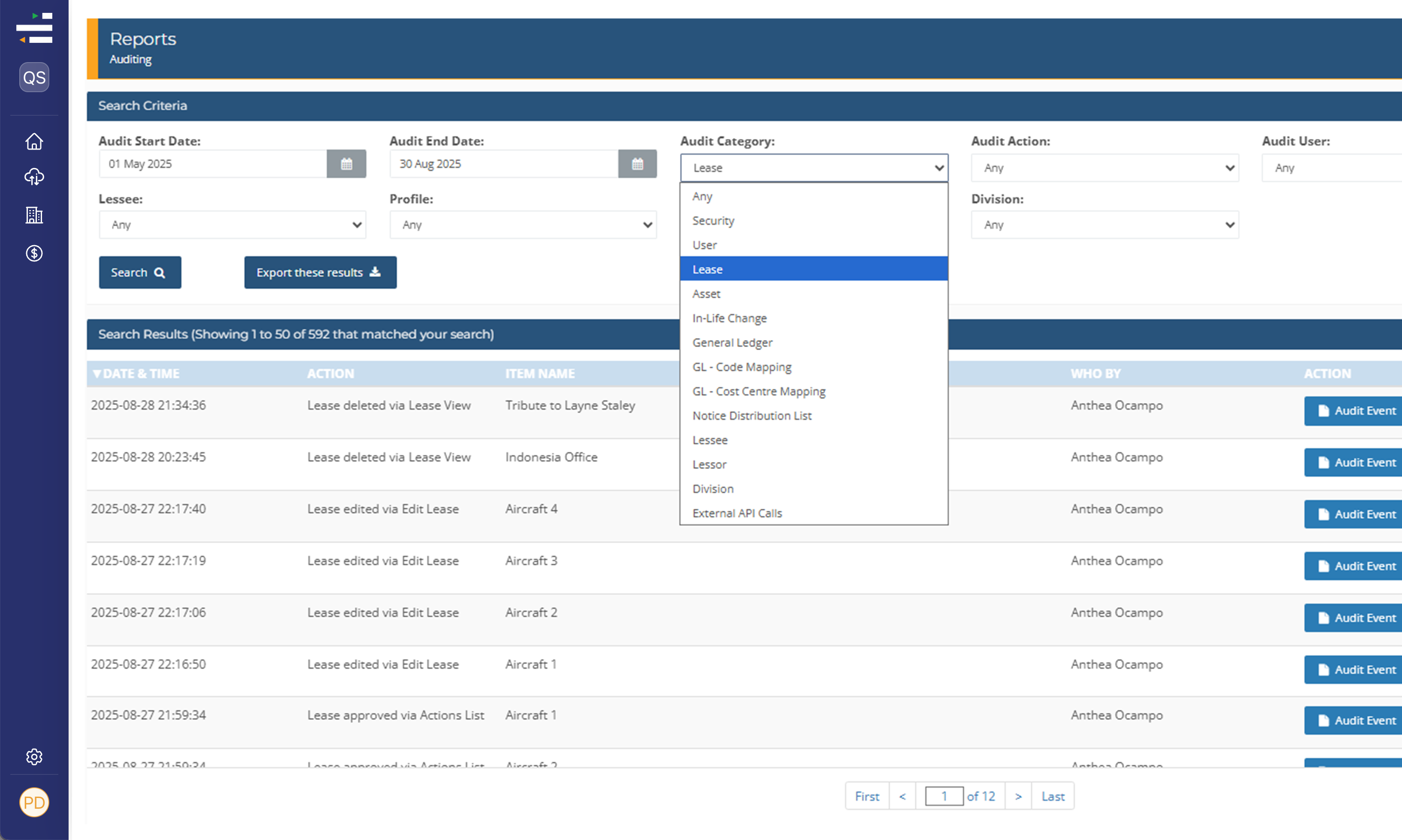

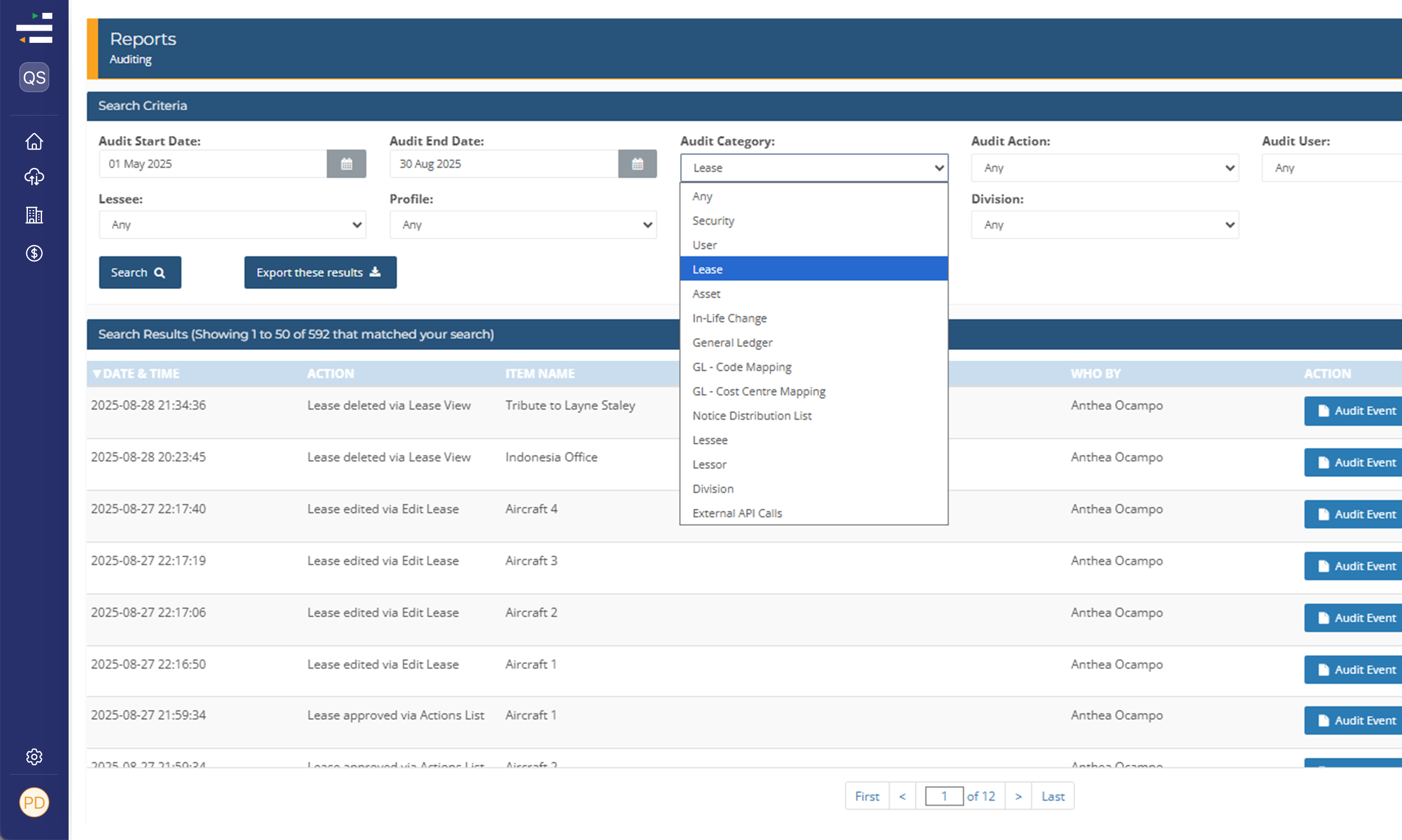

Audit trail and GL

Locked audit trail and general ledger integration

LOIS produces a locked periodic report that agrees the lease subledger to the GL balances automatically, removing the need for a detailed manual reconciliation process. Every journal is traceable from source to output, and every decision is documented, so auditors can follow the evidence chain without extensive back-and-forth.

- Full audit trail for every lease event and modification

- Locked periodic journals ready for GL posting

- Automated subledger-to-GL reconciliation

- Role-based access controls and SSO authentication

- ISAE 3402 assured platform, audited annually

Property and fleet

Property leases, fleet, and embedded leases

Property leases are typically the most material part of any FRS 102 portfolio, and the most complex to manage. LOIS handles multi-site property portfolios with CPI and RPI-linked rent reviews, break clauses, and lease incentives, while a dedicated fleet module automates bulk uploads from any lease provider.

- Multi-site property portfolio management with milestone alerts

- CPI and RPI rent review remeasurements

- Break clause, incentive, and outgoing tracking

- Fleet bulk data upload in any standard format

- Identification support for embedded leases in service contracts

Expert support

Expert-led support from CA-qualified accountants

Maeve O'Connell, LOIS Head of EMEA, brings over 25 years of accountancy experience specifically in leasing finance and FRS 102 transition. The LOIS EMEA team has worked with organisations of every size through accounting standard changes, and provides practical guidance at every stage, from first lease identification through to audit sign-off.

- Dedicated CA-qualified FRS 102 specialist support

- Practical guidance on lease identification and embedded leases

- Transition planning and opening balance review

- Ongoing post-transition support for a changing portfolio

- Optional managed service for full outsourced compliance delivery

Automated FRS 102 Section 20 calculations

LOIS handles every calculation FRS 102 Section 20 requires, with no manual input after setup. The platform computes right-of-use asset values, lease liability present values using the obtainable borrowing rate, depreciation and interest charges, and full amortisation schedules across every lease in your portfolio.

- Right-of-use asset recognition and subsequent measurement

- Lease liability amortisation using effective interest method

- Depreciation and interest split for P&L presentation

- Short-term and low-value asset exemption tracking

- Transition journal entries with no comparative restatement required

Full lease lifecycle and modification management

FRS 102 compliance is not a one-time exercise. Every rent review, extension, scope change, or early termination triggers a remeasurement. LOIS handles each modification automatically, recalculating schedules, generating updated journals, and maintaining a clear rationale trail for every judgement made.

- Extensions, part-terminations, and full early terminations

- CPI and RPI-linked rent review remeasurements

- Indexation and consideration changes

- Rental corrections and impairment records

- All modifications stored with timestamps for audit review

Locked audit trail and general ledger integration

LOIS produces a locked periodic report that agrees the lease subledger to the GL balances automatically, removing the need for a detailed manual reconciliation process. Every journal is traceable from source to output, and every decision is documented, so auditors can follow the evidence chain without extensive back-and-forth.

- Full audit trail for every lease event and modification

- Locked periodic journals ready for GL posting

- Automated subledger-to-GL reconciliation

- Role-based access controls and SSO authentication

- ISAE 3402 assured platform, audited annually

Property leases, fleet, and embedded leases

Property leases are typically the most material part of any FRS 102 portfolio, and the most complex to manage. LOIS handles multi-site property portfolios with CPI and RPI-linked rent reviews, break clauses, and lease incentives, while a dedicated fleet module automates bulk uploads from any lease provider.

- Multi-site property portfolio management with milestone alerts

- CPI and RPI rent review remeasurements

- Break clause, incentive, and outgoing tracking

- Fleet bulk data upload in any standard format

- Identification support for embedded leases in service contracts

Expert-led support from CA-qualified accountants

Maeve O'Connell, LOIS Head of EMEA, brings over 25 years of accountancy experience specifically in leasing finance and FRS 102 transition. The LOIS EMEA team has worked with organisations of every size through accounting standard changes, and provides practical guidance at every stage, from first lease identification through to audit sign-off.

- Dedicated CA-qualified FRS 102 specialist support

- Practical guidance on lease identification and embedded leases

- Transition planning and opening balance review

- Ongoing post-transition support for a changing portfolio

- Optional managed service for full outsourced compliance delivery

Five reasons to choose LOIS for FRS 102

Save time on period-end

Save time on period-end, every period

Finance teams using spreadsheets for FRS 102 face a recurring burden at month-end: recalculating amortisation, adjusting for modifications, checking every figure before journals can be posted. LOIS removes that overhead. Calculations run automatically, journals generate on demand, and reconciliation happens in the background.

Stay audit-ready

Stay permanently audit-ready under FRS 102

Auditors scrutinise FRS 102 the same way they approached IFRS 16: examining how decisions were made, how changes were tracked, and how consistency was maintained across periods. LOIS documents every judgement, modification, and remeasurement automatically. When your auditor asks how a figure was derived, the answer is already in the system.

Manage lease events

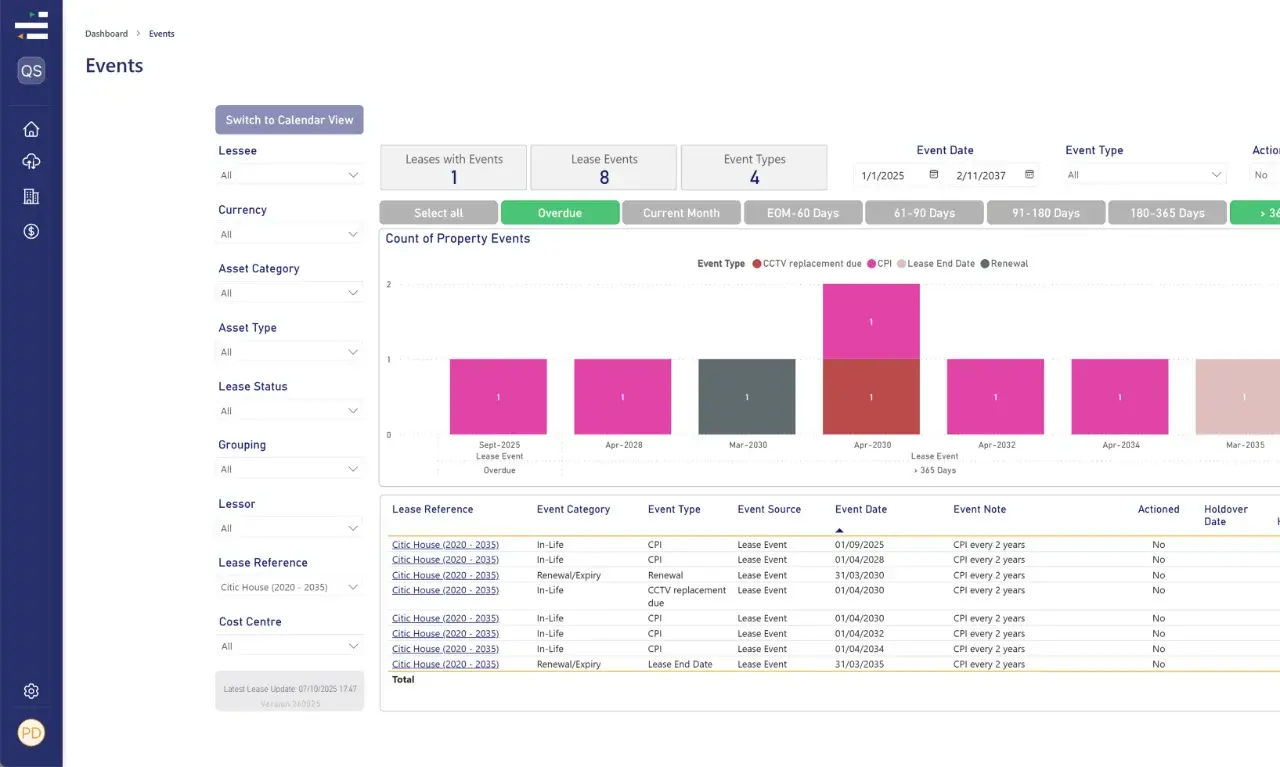

A complete timeline of lease events and milestones

Under FRS 102, every rent review, lease renewal, or modification triggers a remeasurement. Missing one creates a compliance gap that becomes an audit finding. LOIS tracks every event across your property and fleet portfolio, sending automatic reminders before critical dates and logging each action with a timestamp.

Eliminate errors

Eliminate the risk of manual error in a complex calculation set

FRS 102 calculations compound over time. A wrong discount rate at commencement produces a slightly wrong figure every period that follows, accumulating until an auditor finds it. LOIS validates inputs on entry, applies the correct calculation rules automatically, and flags anomalies before they become audit findings.

Reporting you can trust

Reporting your Finance Director and auditors can rely on

LOIS produces disclosure-ready reports, ROU asset movement schedules, lease liability maturity analyses, and reconciliation reports, all locked and traceable. Every output agrees to its inputs, and every input is documented. This is the standard of evidence that auditors now expect from FRS 102 reporters, and it is what LOIS delivers by default.

Save time on period-end, every period

Finance teams using spreadsheets for FRS 102 face a recurring burden at month-end: recalculating amortisation, adjusting for modifications, checking every figure before journals can be posted. LOIS removes that overhead. Calculations run automatically, journals generate on demand, and reconciliation happens in the background.

Stay permanently audit-ready under FRS 102

Auditors scrutinise FRS 102 the same way they approached IFRS 16: examining how decisions were made, how changes were tracked, and how consistency was maintained across periods. LOIS documents every judgement, modification, and remeasurement automatically. When your auditor asks how a figure was derived, the answer is already in the system.

A complete timeline of lease events and milestones

Under FRS 102, every rent review, lease renewal, or modification triggers a remeasurement. Missing one creates a compliance gap that becomes an audit finding. LOIS tracks every event across your property and fleet portfolio, sending automatic reminders before critical dates and logging each action with a timestamp.

Eliminate the risk of manual error in a complex calculation set

FRS 102 calculations compound over time. A wrong discount rate at commencement produces a slightly wrong figure every period that follows, accumulating until an auditor finds it. LOIS validates inputs on entry, applies the correct calculation rules automatically, and flags anomalies before they become audit findings.

Reporting your Finance Director and auditors can rely on

LOIS produces disclosure-ready reports, ROU asset movement schedules, lease liability maturity analyses, and reconciliation reports, all locked and traceable. Every output agrees to its inputs, and every input is documented. This is the standard of evidence that auditors now expect from FRS 102 reporters, and it is what LOIS delivers by default.

Spreadsheets |

LOIS |

|

|---|---|---|

|

FRS 102 Section 20 calculations (ROU asset, lease liability, depreciation, interest) |

|

|

|

Automated lease modifications and remeasurements |

|

|

|

Full timestamped audit trail for every lease event |

|

|

|

Locked periodic reconciliation: subledger agrees to GL automatically |

|

|

|

Automated disclosure reports and FRS 102 Section 20 notes |

|

|

|

Property portfolio: CPI/RPI remeasurements, milestone alerts |

|

|

|

Fleet bulk upload in any format from any lease provider |

|

|

|

CA-qualified expert support and transition guidance |

|

|

|

ISAE 3402 assured, ISO-certified security controls |

|

|

|

Scales from 30 to 10,000+ leases without rebuilding your process |

|

|

|

|

|

|

|---|---|---|

|

FRS 102 calculations (ROU asset, lease liability, depreciation, interest) |

|

|

|

Automated lease modifications and remeasurements |

|

|

|

Full timestamped audit trail for every lease event |

|

|

|

Locked periodic reconciliation: subledger agrees to GL automatically |

|

|

|

Automated disclosure reports and FRS 102 notes |

|

|

|

Property portfolio: CPI/RPI remeasurements, milestone alerts |

|

|

|

Fleet bulk upload in any format from any lease provider |

|

|

|

CA-qualified expert support and transition guidance |

|

|

|

ISAE 3402 assured, ISO-certified security controls |

|

|

|

Scales from 30 to 10,000+ leases without rebuilding your process |

|

|